IoT (Internet of Things) is a buzzword that has been around for a few years and is growing in popularity as we slowly connect everything to the net. An enormous amount of data is being collected already, and this is going to the next level through IoT sensors.

While there are many problems with IoT sensor security that still need to be solved, the data that is being supplied by these devices, if useful and used correctly, has the power to disrupt traditional risk management. This article will discuss some proactive uses of IoT for risk management and why IoT will be invaluable in the finance and insurance fields.

IoT’s Growth

The growth of IoT as a technology is unbelievable. IoT use cases are being seen in nearly every business sector, from connected technologies to cloud computing and digital data. Pharma is using IoT for material tracking and machine monitoring. Oil producers are using IoT for safe extraction and delivery. The travel industry is connecting aircraft to regulate seat temperatures and other IoT devices to make travel seamless.

Cannabis producers are using IoT devices for monitoring their plants from seed to store to stay compliant with their local regulations. Any industry can find benefits from IoT devices. And for finance and insurance, this spread of devices can be used for our own needs.

IoT for Risk Management

The embedding of IoT sensors into physical objects can complement risk mitigation and risk management services. The finance and insurance industries can either piggyback, extracting data from devices that are already installed, or can require the use of our own device’s native sensors. Our goal is to predict and identify risks with reliable accuracy.

During the COVID-19 pandemic, the use of IoT sensors surged in popularity. The shutdowns of the pandemic forced many businesses to rely on IoT sensors to be their eyes and ears.

These new sensors had the ability to watch over vacant buildings. If a building’s system fails, the IoT sensor would identify the failure and notify someone to deal with the problem. The ubiquity of these sensors means that there is a continuous supply of tracking data, like with the data inherent to finance and insurance.

At this year’s Risk Management Society (RIMS) conference, several industry leaders from Waymo, Chubb and Prologis Inc. spoke about how IoT is being used for their risk mitigation practices.

The team members from Chubb, including their chief risk officer, spoke about how IoT is helping Chubb take risk mitigation and management to the next level, allowing them to predict and even prevent potential damage before it happens. A Chubb team member stated that IoT is having a particularly noteworthy impact on their commercial insurance industry. This change is evolving the way that they are now pricing, underwriting, and servicing commercial insurance.

IoT in Insurance

The adoption of IoT in the commercial insurance segment has accelerated significantly since the beginning of the pandemic, and they expect it to expand further. Chubb’s senior vice president and IoT lead, Hemant Sharma, said that Chubb sees IoT as a valuable opportunity to offer their clients bespoke risk prevention services that will ultimately reduce or, in some cases, avoid losses.

Prologis Inc’s senior vice president of global risk management, Jeffery Bray, spoke about how critical IoT was to their business. Prologis has a billion-dollar portfolio of warehouses, and they are using IoT to find better ways to manage and predict risk. IoT tech provides the perfect fit as Prologis’s main risk is driven by property exposure.

The IoT sensors help Prologis get ahead of their operating risks, collect more data in real-time and be more predictive. According to Bray, Prologis is now working on valuing leading indicators as opposed to reacting to lagging counterparts. This switch involves the ideation and development of “autonomous” buildings, those which effectively use IoT devices.

One new area advancing IoT: drones. After a natural disaster, drones can be utilized to gather in-field data quickly for any resulting claims. Drones gather data for building inspections, providing underwriters with more information and people with faster payouts.

Potential Uses for IoT in Risk Management

For future uses of IoT, there are two crucial questions to ask:

1. Will this new technology help drive differentiation in the marketplace?

2. Will it stand the scrutiny required of a solid and profitable business case?

The risk management space has many candidates that can potentially fulfill these requirements.

Oil and Gas

The oil and gas industry has consistently invested in its sensor and early warning infrastructure to ensure safety. Some of the most common risks in the energy industry are injuries, fires, hazardous gas leaks, and vehicle accidents.

A collaboration between the energy industry and insurers can be formed through IoT data to look for the early signs of potential accidents. This can prevent costly accidents, environmental spills, and insurance claims.

Despite preventive measures, risk is always present with oil and gas, and the costs of adverse events are often devastating. Research from 1974 to 2015 shows the total accumulated value of the 100 largest oil and gas disasters exceeds $33 billion. Another report shows that only Russian refinery damage from 2011 to 2015 exceeds $1.5 billion.

Infrastructure

The variety of sensors for commercial infrastructure OEMs has seen a substantial increase. These sensors can monitor safety breaches, ranging from water leakage, smoke, overloading of weight-bearing structures, and the presence of mold and mildew, among others. There will be an ongoing integration of infrastructure management systems with IoT data to aid loss prevention programs and provide preventative actions.

A 2018 study compared a classical (non-telematics, IoT-based) risk model against a telematics-based version and a hybrid (telematics and traditional factors) version, measuring their predictiveness levels. The result: the classic model ranked least predictive.

Grocery and Other Retail

With the millions of routine visits to these stores and the potential hazardous locations within grocery and convenience store aisles, seafood facilities, salad bars, and liquid storage areas, opportunities for proactive risk management are abundant.

IoT devices can be used in accident-prone areas to monitor human traffic patterns, debris, and cleaning. Beyond the logging of activity for compliance reasons, IoT can help prepare injury reports and the necessary remedial actions for reducing claims-based losses.

Smart Homes

We now see the addition of new connected devices entering our homes. Ring doorbells, smart thermostats, baby monitors, IoT-enabled refrigerators, other appliances, pipe leakage sensors, lighting, and entertainment controls are becoming more commonplace. If utilized correctly, the resulting increase in data can allow for new innovative insurance products and engagement with the insured and mortgage borrowers.

Wearables

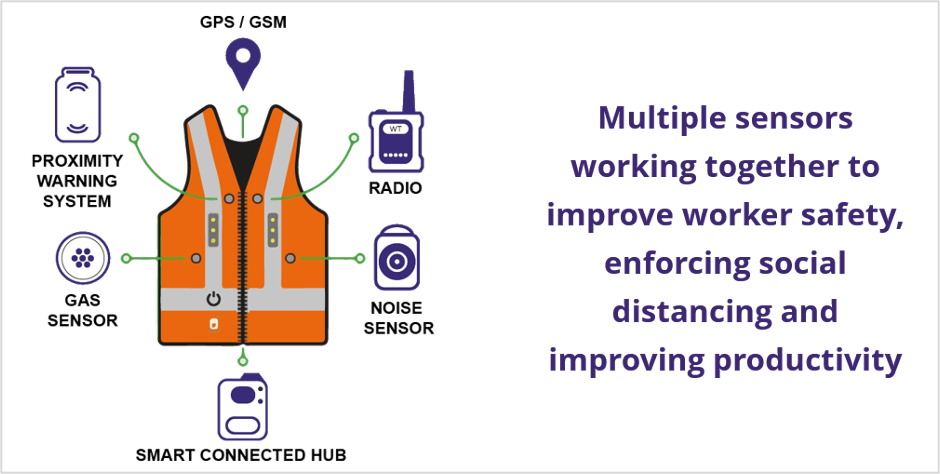

Connected health wearables such as watches, patches, shoes, socks, and a new supply of industrial safety wearables are entering the market.

These different items of clothing monitor biometric data, as well as odd joint angles (improper lifting technique, carpal tunnel syndrome), bad posture, and more. They help prevent injuries and costly medical insurance claims.

Proactive Risk Management in IoT Programs

IoT technologies continue to evolve, and the real test is whether the technology can benefit the finance or insurance carrier and the borrower or insured respectively. Until the industry can get a high engagement index with the user, be they personnel or commercial, the chance of the user opting out remains high. Thus, the technology’s potential is limited.

Progressive Insurance and other pioneers in the IoT space have moved in the right direction, initially focusing on the automotive sector. Their Snapshot program rewards the insured with monetary benefits when they can drive safely and avoid high-risk driving behaviors such as late-night driving or excessive acceleration and breaking.

The result is a “high stickiness” describing their insured population, who will keep lower rates for passing the six-month “Snapshot” test. It also allows Progressive to identify more risky drivers that will not receive the lower rates while still notifying those drivers with “beeps” that their actions are hazardous. Additionally, Snapshot has withstood the scrutiny of actuaries, reshaping how insurers assess, limit, and price the risk of their product offerings.

So, what can we do to fulfill the two questions of market differentiation and profit?

- Develop an ecosystem with technology partners. This means to explore the IoT marketplace thoroughly by studying product roadmaps, vendors, and system integrators.

- Continuously experiment. This means to include businesses and markets adjacent to your usual targets through expanded coverage or product rehauls.

- Integrate IoT into operations early. In other words, developers must marry underlying systems to IoT-capable devices starting from the ideation stage.

- Plan for the long-term. As IoT evolves, business leaders should increasingly take on an “investor mindset,” seeking out opportunities to improve income or reduce costs?

Closing Thoughts

The internet of things (IoT) is flourishing globally as the number of connected devices continues to expand, projected to grow beyond $50 billion in 2025, with more than two devices for every human (19.1 billion). This massive expansion, coupled with ongoing device computing power improvements, is giving rise to new possibilities for the finance and insurance industries..

Possible incentives include better pricing on mortgages and loans, rebates on policies, and discounts for companies that use them. IoTs also come with added conveniences, such as reduced employee absence, less downtime, and faster repairs. The key is to remain proactive and consistently seek out methods by which IoT reshapes the global risk management industry.

Disclaimer: The information provided in this article is solely the author’s opinion and not investment advice – it is provided for educational purposes only. By using this, you agree that the information does not constitute any investment or financial instructions. Do conduct your own research and reach out to financial advisors before making any investment decisions.

The author of this text, Jean Chalopin, is a global business leader with a background encompassing banking, biotech, and entertainment. Mr. Chalopin is Chairman of Deltec International Group, deltecbankstag.wpengine.com.

The co-author of this text, Robin Trehan, has a bachelor’s degree in economics, a master’s in international business and finance, and an MBA in electronic business. Mr. Trehan is a Senior VP at Deltec International Group, deltecbankstag.wpengine.com.

The views, thoughts, and opinions expressed in this text are solely the views of the authors, and do not necessarily reflect those of Deltec International Group, its subsidiaries, and/or its employees.