Bitcoin, Ethereum and most other crypts are powered by a technology called blockchain. A blockchain, quite simply, is a list of transactions (a ledger) that anyone can view or verify. Bitcoin’s blockchain, for example, contains a record of every instance someone sent or received any bitcoin.

The blockchain technology that powers cryptos makes it possible to transfer value online without a centralized and trusted intermediary, such as a bank or credit card company.

With this article, we hope you will see the potential of blockchain, an open alternative to nearly all the financial services you use today, as well as a broad range of other possibilities accessible to all with a smartphone and internet connection.

Image courtesy of prfinancialnews.com

Image courtesy of prfinancialnews.com

Starting With Bitcoin

Bitcoin’s Genesis Block was the first instance of a blockchain system and is the grandfather for all other blocks in its blockchain. This Genesis Block was created in 2009 by Satoshi Nakamoto, Bitcoin’s pseudonymous developer, who may be an individual or group, and whose identity is still uncertain.

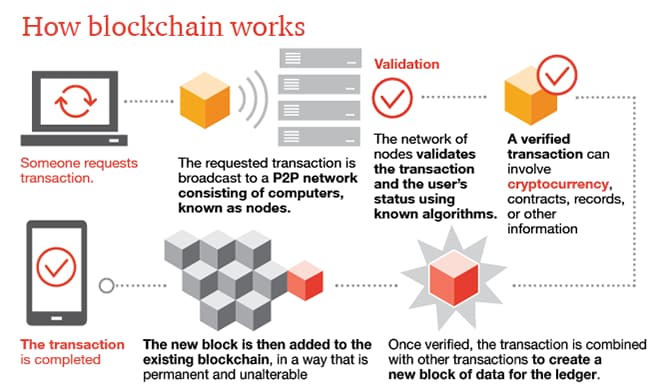

Bitcoin’s blockchain is a globally distributed ledger of data blocks that are sequentially linked to form a chain. Each block of the chain has information about the previous block and information about the new transactions that are added to the chain.

If you follow the Bitcoin chain backward, you will eventually arrive at its Genesis Block. Multiple copies of the chain’s data are stored by “miners” in distributed nodes rather than in a single location or server.

This system would make the substitution of the records nearly impossible unless over 50% of the nodes were changed at once. The blockchain also includes a locked set of protocols that govern the flow of data between the network of nodes.

Image Courtesy of PWC

Image Courtesy of PWC

{kind=link}

When combined, these attributes give the Bitcoin blockchain as well as altcoins powerful security advantages. Blockchain means an open and transparent ledger of the cryptocurrency’s history. Manipulating a blockchain transaction will be unsuccessful because it causes the chain not to link and break, notifying the entire system of nodes that something nefarious is going on.

Two Blockchain Parties

Users

Users are the owners of bitcoin wallets, and the two things they can do are receive and send bitcoin. For other blockchains, the complexity of information that can be sent and received is increased but for our purposes, the process of transfer is nearly the same. A user will broadcast their data (for a transaction) to the Bitcoin (BSV) network. When this arrives, the network will validate it and add it to a list of pending transactions. A digital signature confirms the transactions authenticity (the sender is who they say they are), adding this layer of security to the transaction. A fraudulent transaction could be signed, but the signature would also be proof of fraud. Individual transactions from the pending transaction list will be grouped and form a cryptographically secured new block for the chain.

Miners

These are the computers doing the work of the transaction behind the scenes. The blockchain’s protocol defines how data is organized into each new block. This new block’s information, which is the new transaction information, a timestamp, and information from the previous block, in the form of a long chain of numbers called a “hash,” created from the previous block’s data. Then the chronologically sequential chain has the most recent block added. Every miner on the network maintains a copy of the entire blockchain’s data, verified on an ongoing basis.

The Miners maintain the network and confirm the authenticity of the ledger transaction with a consensus mechanism. The two most common mechanisms are Proof of Work (PoW) and Proof of Stake (PoS). With Bitcoins PoW consensus mechanism, miners use energy competing to solve a mathematical problem to validate the authenticity of the block’s transactions. The double-spending problem (sending the same bitcoin to two different accounts) is prevented because miners will reject a block with any double-spending. The fastest miner to authenticate a block will receive a reward for that block of new bitcoin. Once found, the solution is shared with the other miners to solidify the block onto the chain and move on to the next block and its reward. A shared history is available for the network miners to avoid entry duplication and ensure miners have the latest version.

Any attempt to alter an earlier created block would result in a different hash for the subsequent block and therefore not match. With all nodes having a copy, the tampering would be identified, and for this reason, a chain with matching hashes can be trusted. Therefore, the Bitcoin blockchain is beyond the control of any single person, company, or even country (though some companies and governments have developed their own blockchains).

Why is blockchain a big deal?

With no need for a central authority, blockchain transactions are an ideal settlement solution. They are removing the need for a settlement agent like a clearinghouse. This change reduces the costs and can potentially increase the speed of transactions if a blockchain if sufficiently scaled. Additionally, being decentralized, if one part of the system goes down, a blockchain network remains functional. Finally, there is security; being decentralized with an open system of cryptographic blocks that incorporate the previous block’s hash, the blockchain’s users can trust each other for peer-to-peer transactions while also not having to provide identifiable financial or personal data that could be used for identity theft.

Take, for example, a credit card. An online credit card transaction involves filling in significant identifiable data, including the cardholder’s name and address, card number, expiration, and CVC number. That information is then transferred to a merchant that sends the info to a central clearinghouse that processes the transaction (for a 2-4 plus percent fee). All along the way, there are opportunities for problems:

- The merchant may steal the info

- A hacker may intercept the information between you and the merchant or between the merchant and credit card processor

- Incorrect information may be used (wrong order, wrong card)

- A hacker or employee or even a bug in the system can change the credit card company’s ledger

- The centralized system can go down, preventing transactions

- Numerous other issues such as backup discrepancies

Nearly all these issues are eliminated with blockchain and for a fee currently between 2 and 3 dollars which with scale, should continue to fall.

Uses of Blockchains

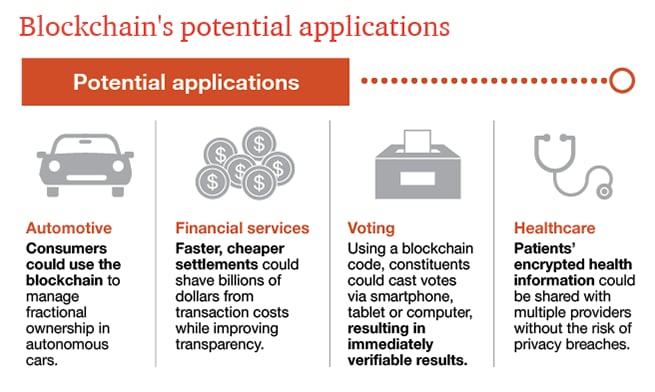

With all blockchains, their data is stored and signed publicly; a transaction signing demonstrates its possession while the encryption provides accessibility. This simple yet ingenious structure allows for much more than transferring value or control rights across several applications and industries. The ability to authenticate and authorize any transaction is possible with blockchain. A system of smart contracts has been developed for most notably the Ethereum network, which can define both rules and penalties for an agreement just the same way as a traditional paper contract. If all the requirements and conditions of a contract are fulfilled, then the transfer of the item in the contract is automatically done, and there is a public record of it. This system solves several legal issues, builds trust, and removes intermediaries from many forms of commerce. Blockchains have been used to improve medical record accuracy, in medical research, voting, the ownership of art and as a form of art itself in the form of NFTs, and the streamlining of supply chains, to name a few.

Image courtesy of PWC

Image courtesy of PWC

{kind=link}

Summary

Blockchain’s rise in popularity comes from three significant advantages over legacy financial systems. It has better security, it allows for trustless transactions between anonymous parties, and its structure reduces transaction costs by removing intermediaries. While the crypto space remains the while west for investment, the blockchain technology that makes up its foundation is solid, and we are now seeing the best uses of it emerge for all. Blockchain will continue to evolve and bring us more efficient solutions to current systems as well as provide avenues to unforeseen products and services.

Disclaimer: The author of this text, Jean Chalopin, is a global business leader with a background encompassing banking, biotech, and entertainment. Mr. Chalopin is Chairman of Deltec International Group, deltecbankstag.wpengine.com.

The co-author of this text, Robin Trehan, has a Bachelor’s degree in Economics, a Master’s in International Business and Finance, and an MBA in Electronic Business. Mr. Trehan is a Senior VP at Deltec International Group, deltecbankstag.wpengine.com.

The views, thoughts, and opinions expressed in this text are solely the views of the authors, and do not necessarily reflect those of Deltec International Group, its subsidiaries, and/or its employees.