We have an economy that is now switching to 5G, and in a few more years, we may even see 6G speeds. However, the global economy’s digital transformation is far from complete. After our struggles with Covid-19 affecting both health and commerce, we have moved our world toward global, digital connectivity. For example, digital wallets will forever transform the way that we bank, shop and pay.

Most of the world, including developed economies, is still only in the early stages of a true digital transformation. We will look at the future of digital wallets and see how they are going to be an integral part of the comprehensive digital potential that is coming to all of us. The new connected economy will be defined by several pillars, all affecting our daily lives.

Digital Wallets

Digital wallets allow their owners to store and spend funds digitally in the form of “real” money linked to a debit, credit, gift card, coupons, or loyalty points. Digital wallets differ from other online payments because they allow the user to save payment information by adding their card or account information to the app. When payment is required, the buyer can do it straight from the app, only needing to hold the smartphone close to the reader, and not having to remember or enter payment credentials.

This is only the start of digital wallet capabilities. Digital wallets can do much more, from adding loyalty cards, airline boarding passes, movie tickets, hotel door keys, and more. The recent growth of this technology has allowed many to leave bulky wallets behind and has pushed our economy toward cashless payments.

Apple, Samsung, and Google have all integrated these wallets into their devices and have become the biggest players in the space. Retailers like Walmart and Alibaba have added digital wallet capabilities to their checkouts, and PayPal, Cash App, and Venmo, which offer digital wallet services, have grown into financial powerhouses.

Banking’s Future

Beyond the convenience digital wallets provide at checkout, they can potentially solve the cross-border banking problem, a difficult-to-navigate and disjointed process. Opening an international bank account is often long and painful, and international transfers can add more roadblocks and delays lasting days or more.

New Fintech firms allow businesses to open their own international accounts with multicurrency IBAN in the organization’s name. Virtual wallets then make the process easier with same-day payments, while the company can keep funds in multiple currencies allowing for prompt payments and currency exchange.

The Technology of Digital Wallets

Digital wallets start with a digital core. This is obviously the foundation behind the digital transformation of banking. And this digital core refers to the applications and platforms a financial institution utilizes in its transition to a digital business.

It then uses open APIs (application programming interfaces) to integrate payment platforms and digital wallets, which bring front-end benefits to its consumers. With these fundamentals, institutions can build services that effectively and directly communicate to clients, driving transformational change. There are already many popular crypto wallets in Europe, Asia, and the Americas–nearly the whole world.

Beyond the open APIs, we will see more smart ledgers and wallet management programs come forward. These blockchain-based smart ledgers will transform the handling of digital wallets. Offering a way to record, transfer, and store alternative assets in token form, adding to digital wallet capabilities. When combined with API-accessible wallet management, users will experience a fully integrated digital payment model within a single platform.

Crypto’s Potential

The rise of cryptocurrencies is still considered an untapped frontier of digital wallets. Trading these non-tangible digital currencies has increased, and the price of a bitcoin has risen from $1 in 2011 to tens of thousands today. Remaining speculative means that crypto is ripe for continued growth, and the push for CBDCs means that the banking sector is concerned. It’s even possible to use APIs for algorithmic trading.

Visa is hedging its bet, building the structures for CBDC integration and for its own crypto digital wallet. This institutional interest and strong demand across wealth management are apparent, and there is a significant blockchain product offering that has the potential to transform the way markets behave. The blockchain value proposition has shifted to what else a blockchain can do beyond store value.

Digital Wallets Connect Economies

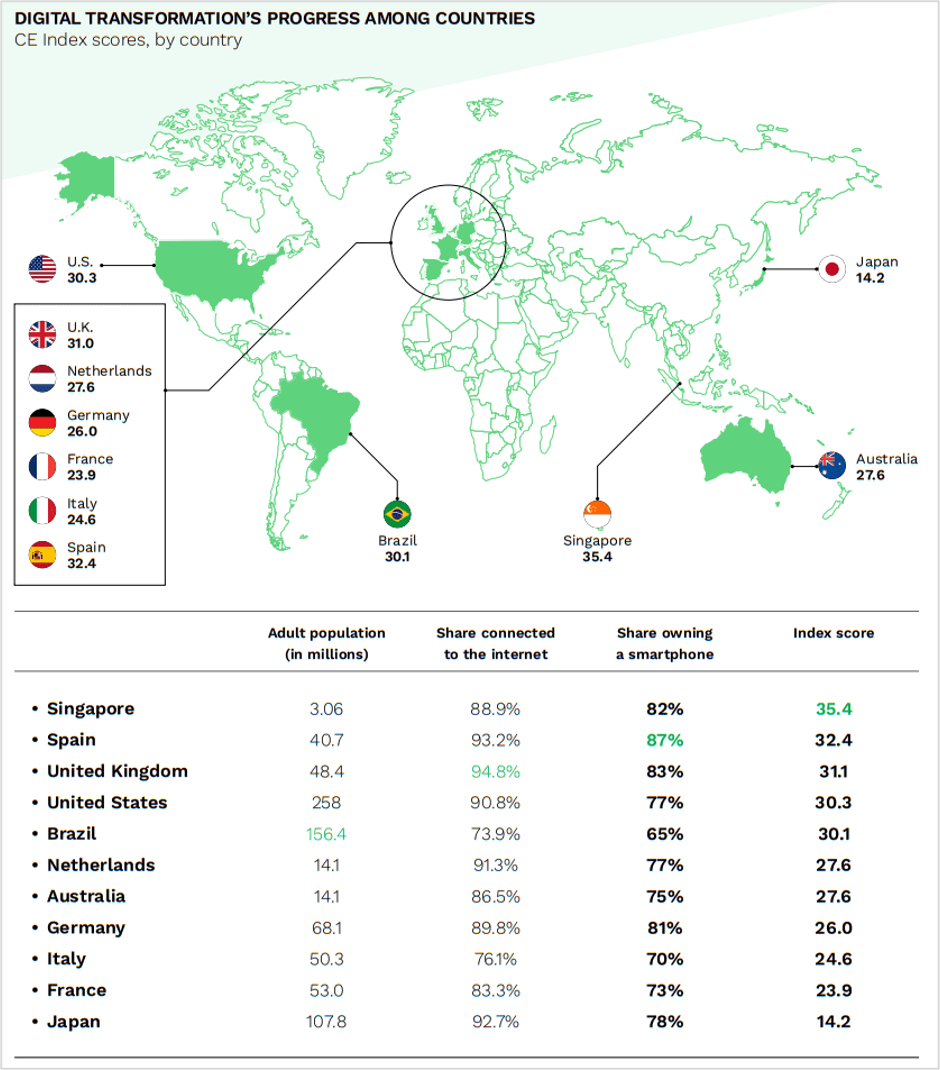

In a report about the connected economy by Stripe and PYMNTS, which surveyed over 15,000 participants from 11 countries, the ongoing digital transformation has only reached about a quarter of its full potential across those studied. These 11 countries represent about 500 million adults, a small portion of our now 8 billion global population.

{kind=link}

Brazil and other developing countries have massive potential to grow their connected stature. But even in highly connected places such as Spain, the UK, and Singapore, only about one-third of their digital connectedness has been achieved. The untapped potential hints that there are roadblocks to be overcome and transformation to be had.

Streaming and Social Media

On average, the survey found that 87% of respondents were connected to the internet. However, fewer than 20% were highly engaged with digital activities, especially shopping. This is an interesting, ironic result of the slowing but persistent pandemic. However, streaming services are the exception.

The research found that seven times as many consumers are engaged in watching streaming videos daily on YouTube, HBO or Netflix as are shopping on a marketplace like Amazon, Etsy, or eBay. Social media is the other plus point, with five times as many consumers checking their social media as compared to ordering food.

Digital Wallet Use Is Here to Stay

Digital wallets are the key to this connected future. Covid-19 brought a growing embrace of touchless or contactless payments, speeding up digital wallet adoption. There is no clear digital wallet leader, and use patterns differ based on geography.

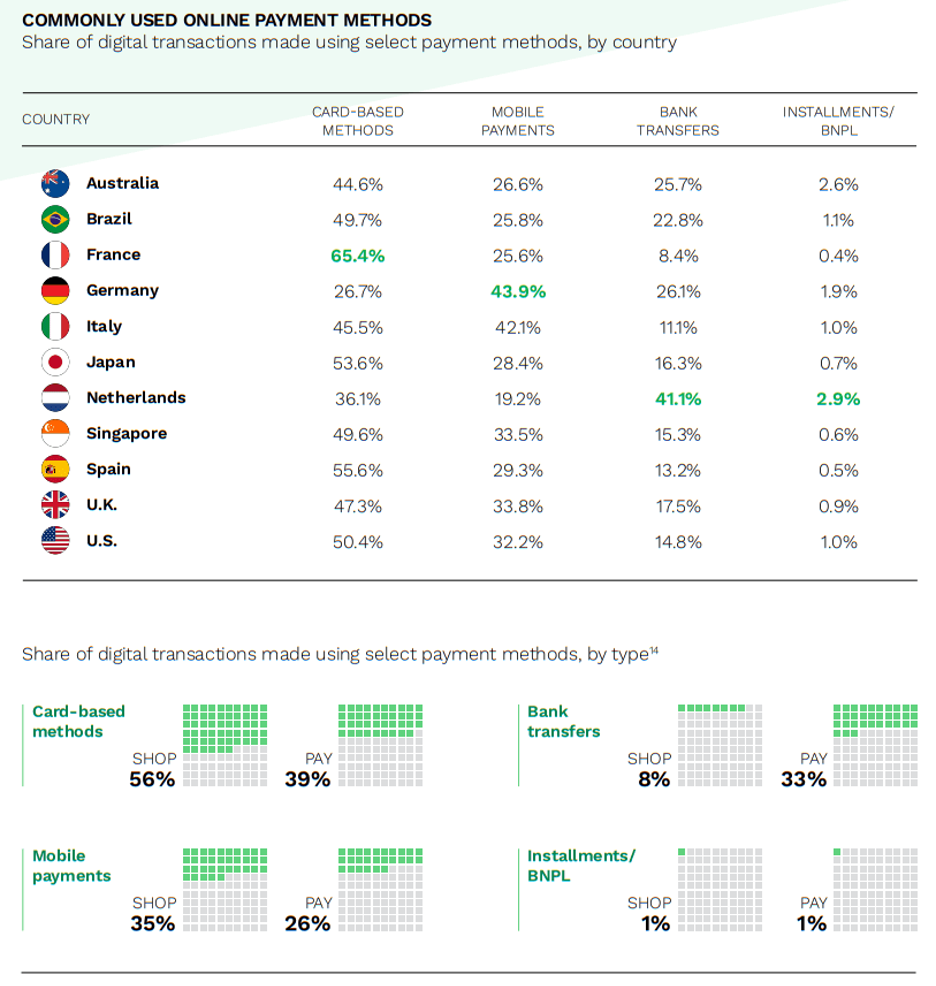

PayPal is commonly used in the most digital wallet-centric nation, Germany, accounting for 37% of all online transactions. More than 40% of all domestic online transactions in Germany are using digital wallets, with 84% of these using PayPal.

In 2019, mobile wallets surpassed credit card use globally, becoming the most widely used payment type.

Juniper Research predicts that the number of unique digital wallet users will grow from the current 2.6 billion to 4.4 billion by 2025. China and India will lead the way, accounting for nearly 70% of all digital wallet transactions, with the US and UK lagging in digital wallet adoption.

Digital wallets have been successful in areas with low card penetration but high phone use. Southeast Asian consumers skipped cards, going from cash to mobile wallets, and digital wallet providers have done exceptionally well.

With this adoption of digital wallets and newer forms of digital currency, cryptocurrencies or CBDCs will be in demand. Future digital wallets will seamlessly store and pay in several currencies, particularly as many retail online brokerages offer crypto and checking accounts.

Closing Thoughts

As we become digitally connected, digital wallets play an obvious, necessary role. Their reach will spread, and governments and companies will push for their continued use. The increase in services they will supply, solving cross-border transaction issues, and improving the ease of banking will ensure that we use our digital wallets when we bank, shop, and pay.

Other services should look to digital streaming and social media to see how we can better integrate digital payments and digital connectedness into our lives. China and India will continue to lead this march, but that doesn’t mean the West shouldn’t catch up quickly.

Disclaimer: The information provided in this article is solely the author’s opinion and not investment advice – it is provided for educational purposes only. By using this, you agree that the information does not constitute any investment or financial instructions. Do conduct your own research and reach out to financial advisors before making any investment decisions.

The author of this text, Jean Chalopin, is a global business leader with a background encompassing banking, biotech, and entertainment. Mr. Chalopin is Chairman of Deltec International Group, deltecbankstag.wpengine.com.

The co-author of this text, Robin Trehan, has a bachelor’s degree in economics, a master’s in international business and finance, and an MBA in electronic business. Mr. Trehan is a Senior VP at Deltec International Group, deltecbankstag.wpengine.com.

The views, thoughts, and opinions expressed in this text are solely the views of the authors, and do not necessarily reflect those of Deltec International Group, its subsidiaries, and/or its employees.