With “the Merge” to Ethereum 2.0, the world’s second largest blockchain network by market cap has been the talk of the town. We have heard and read some postulating that Ethereum (ETH) can succeed even if it does not scale correctly.

The ETH is more than its potential scalability. It stores billions, and eventually, trillions in value and does not need a central monetary authority or bank. However, the necessary key is increased liquidity and decreased volatility.

Bitcoin (BTC) has followed a similar path to Ethereum, with many saying they wanted the BTC network to scale as a priority. They believe that Bitcoin’s success is measured as a rival for Visa, or it will fail, arguing that it must be a method of exchange rather than only a “Store of Value” like gold.

This requirement results in a decentralized network in jeopardy, prone to censorship and government capture. Fortunately, even with the high cost of mining hardware, small block miners have been successful. At the same time, network scaling is happening through “layer-2” (outside the base blockchain layer) solutions and side chains like Liquid and the Lightning Network. And Bitcoin’s base layer can keep its role as an SoV while building its own exchange network.

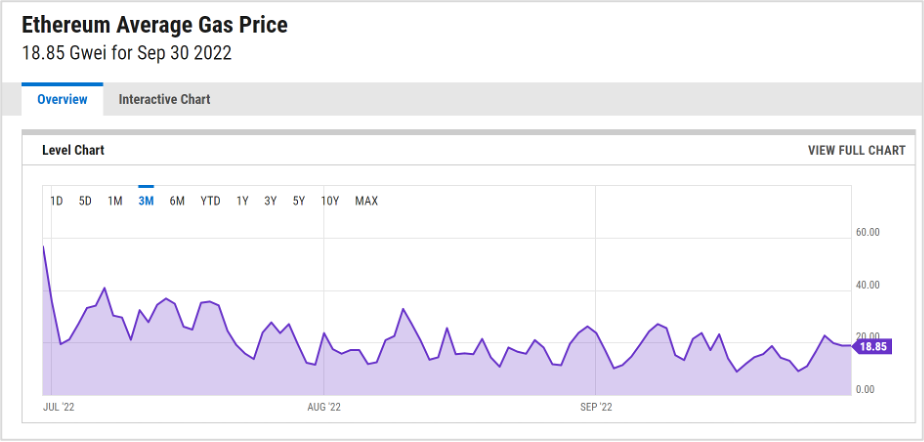

Ethereum is designed to be the world’s computer with unstoppable code that can run Dapps cheaply and trustlessly. But Ethereum has had to implement a major fix since the DOA hack, forgoing decentralization, and scalability was also jeopardized when the Dapp CryptoKitties broke the chain’s usability. We hope that Ethereum’s move to proof of stake will solve the throughput issues and lower the gas (transfer) fees for base-layer transactions which can be excessive.

Since Ethereum’s Merge, the supply of new ETH is slowing. According to data from Ultra Sound Money, the Ethereum issuance rate has fallen by 98%. Though it has not become deflationary. At the end of September 2022, it is only sitting at 0.09% annualized growth per year with a total of 14,042,583 ETH currently in Ethereum staking contracts, totaling $18.7 billion.

Ethereum Is Not Decentralized

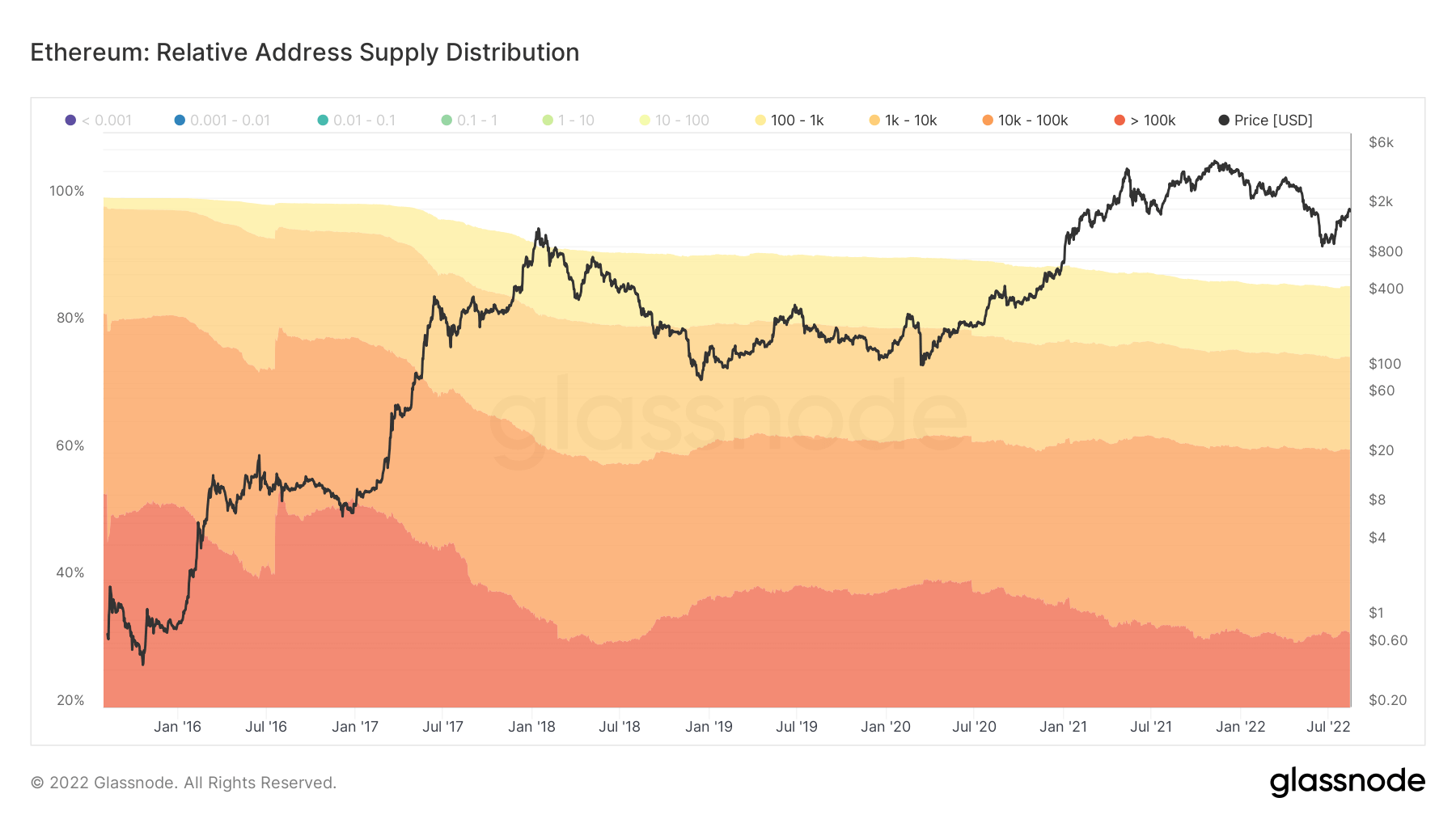

Glassnode data shows that 85% of Ethereum’s total supply is held by entities that have 100 ETH or more, and 30% of the supply is in the hands of (wallets of) those with over 100,000 ETH.

{kind=link}

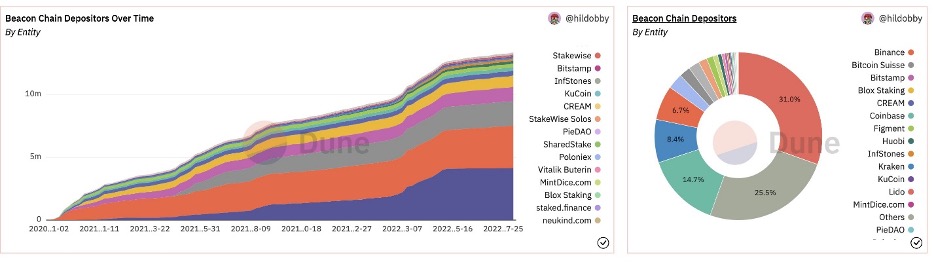

Ethereum’s centralization issue is even more apparent with the shift to proof of stake. Being a “staker” does not require the same hardware as proof of work, but a validator needs to have 32 ETH staked to participate, a sum that most cannot afford. Ethereum’s “Beacon Chain” validators illustrate how the PoS system will look.

Most Beacon Chain validators are large entities, large exchanges, and newly founded staking providers with significant ETH holdings. A large portion of validators are legal entities registered in either the US or the EU, subject to those jurisdictions’ regulations.

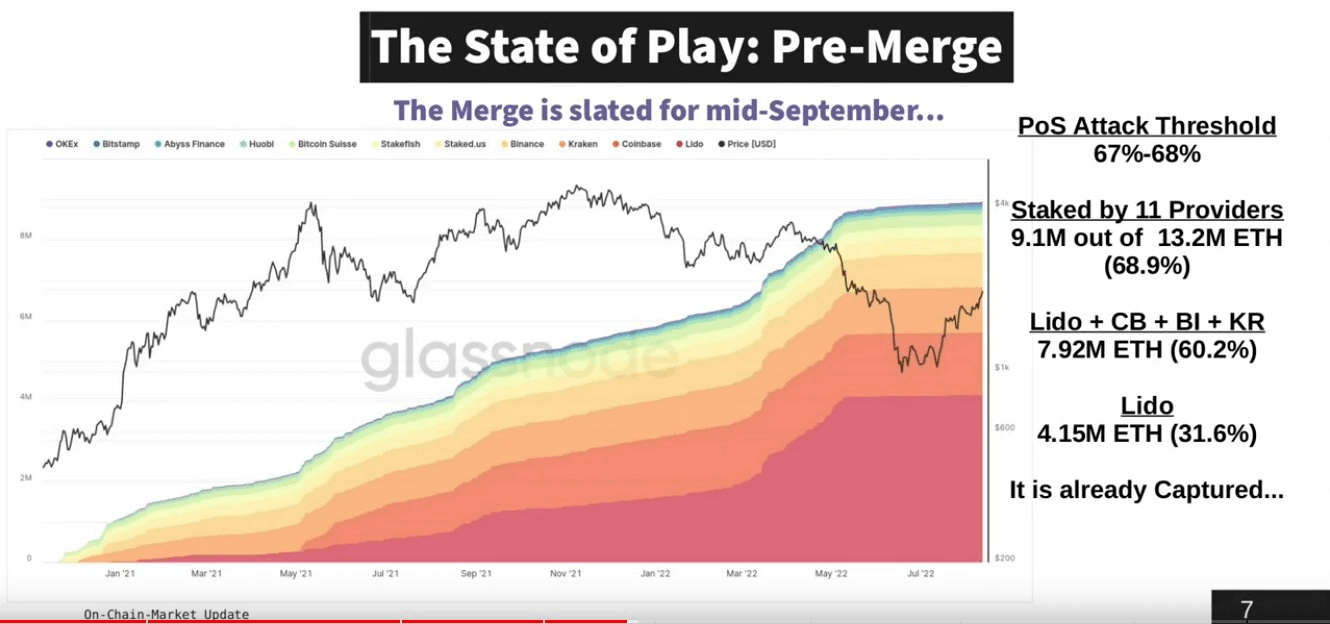

These centralized holdings mean that just under 69% of the total amount of ETH staked on the Beacon Chain is held by a mere 11 providers, with 60% staked by only four providers. A single provider, Lido, makes up 31% of the staked supply.

When there is a bull market like we saw until the first quarter of 2022, this amount of centralization generally goes unnoticed, but as the tide turns, uncertainty reveals such flaws.

The potential for a proof of stake attack is just under 68%, and if the top 11 stakers were to collude, they could succeed in such a play.

{kind=link}

No Really, DeFi Is Centralized Too

Decentralized finance was never really decentralized in the first place. The truth is that Ethereum’s not securing as much decentralized wealth as we think. Much of the value of Ethereum is in yield farming that results in high annualized yields, and in other Ethereum-based DeFi that worked until 2022’s crash. High yields had prevented major players from looking behind the curtains and finding the flaws.

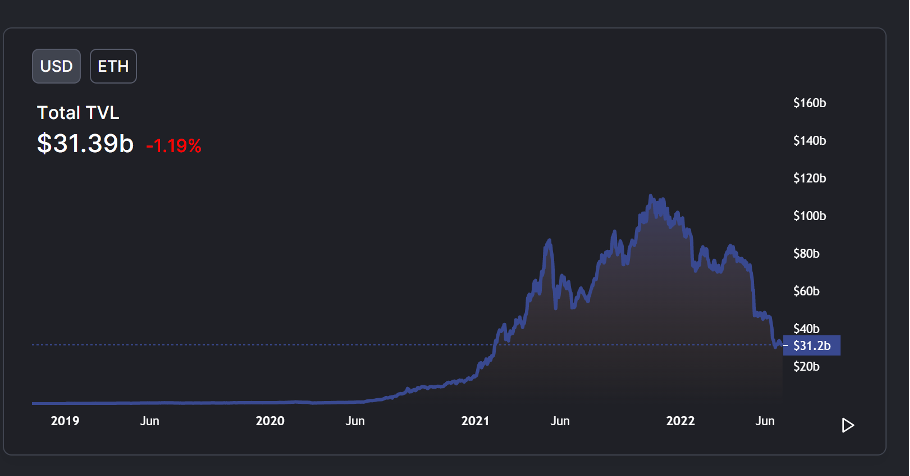

There was a massive growth in the “Total Value Locked” (TVL) of Ethereum, but since the crypto is not actually locked—it is temporarily deposited to capture those ridiculously high yields, hence dropping from $110B to $31B in only a year.

Lack of Users

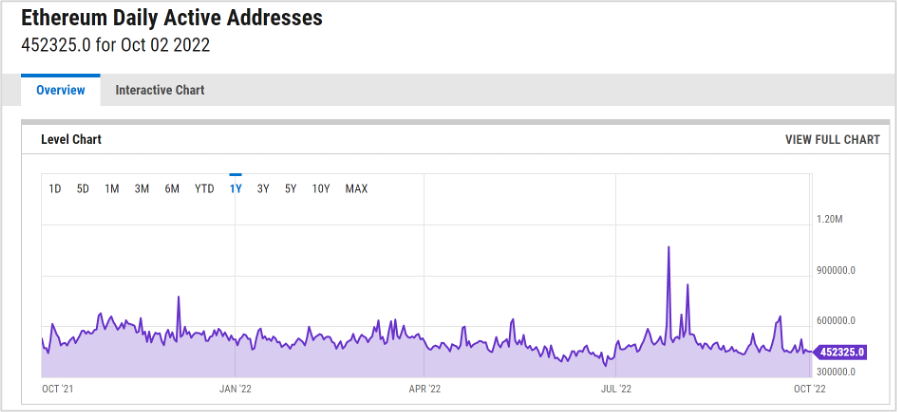

Likely fewer than 500,000 people have interacted with DeFi or with Ethereum. The user numbers for YCharts, DappRadar, DefiPulse, Etherscan, and Nansen, are all underwhelming.

While the most valuable Ethereum-based DeFi coins have a small number of active users, it means that their fees are high enough to drive new users away from Ethereum. The highest valued DeFi protocols only have users in the thousands (OpenSea has only 26K daily users; see above). The reason that $31 billion is “locked” is the incentive of high “APY” (yield) liquidity mining.

When users are being paid to borrow money from a DeFi protocol, you cannot consider any one user the same as a long-term holder. They can disappear quickly.

The Solution

The solution for a centralized system is quite simple–make it more decentralized. Unfortunately, those currently working on Ethereum are rebuilding everything that is wrong with Wall Street and putting it on a blockchain.

The deep-pocketed backers or in-the-know developers are pushing for centralization because they desire the most of the pie. As limited as Bitcoin is functionally, it is the most decentralized cryptocurrency with the prevalence of Bitcoin’s fractional shares. However, Ethereum has more potential and can be successful.

Staking

Staking was intended to remove the hardware requirements that kept the small player from participating. The requirement of a 32 ETH stake for participation in PoS is limiting. In October 2022, 32 ETH is about $44,000.

If there are enough decentralized staking pools, then much of this issue can be resolved. By allowing many to invest through aggregating pools, the small players can finally join in.

Layer-2 and Beyond

If the number of nodes (validators) is high enough to lower the gas fees and increase the throughput of ETH, then Ethereum may have a successful decentralized future. If other avenues imprinted on Layer-2 solutions can increase the affordability of transactions further, enabling micropayments like what µRaiden wants to do, then Ethereum can be truly decentralized. This may draw much more retail, everyday users to cryptocurrency through the many American or European crypto exchanges.

When combining affordable layer-2 solutions with a broad and decentralized PoS system, Ethereum will lose much of its centralization.

Volatility and the Catch-22

The use of ETH is the key, but volatility is the restriction. While the types of price swings we have seen in the crypto markets remain (10% or more in a day), all crypto use will be limited. The problem is that while the volatility is high, the acceptance will not be widespread, and while acceptance is not widespread, volatility will be high.

Getting transaction prices down and making micropayments possible will allow for more widespread use, and more widespread use means more stability. If the large holders can release their grip that is centralizing Ethereum, then they will likely do better in the long run for the greater good of decentralization.

We are incredibly positive about the Ethereum network and look forward to its decentralization.

Disclaimer: The information provided in this article is solely the author’s opinion and not investment advice – it is provided for educational purposes only. By using this, you agree that the information does not constitute any investment or financial instructions. Do conduct your own research and reach out to financial advisors before making any investment decisions.

The author of this text, Jean Chalopin, is a global business leader with a background encompassing banking, biotech, and entertainment. Mr. Chalopin is Chairman of Deltec International Group, deltecbankstag.wpengine.com.

The co-author of this text, Robin Trehan, has a bachelor’s degree in economics, a master’s in international business and finance, and an MBA in electronic business. Mr. Trehan is a Senior VP at Deltec International Group, deltecbankstag.wpengine.com.

The views, thoughts, and opinions expressed in this text are solely the views of the authors, and do not necessarily reflect those of Deltec International Group, its subsidiaries, and/or its employees.