When we have assets and debts, there are two conflicting things going on. Our assets are growing in value while our debts are accumulating interest. Enter: self-paying crypto loans.

Imagine if loans had no interest. Instead, the appreciation of your assets is automatically going to pay off your debts. Your mortgage payment is automatically paid off by your stock portfolio’s growth, and a car payment is paid by the funds of your high yield savings account. Your credit cards are paid off by your real estate portfolio, and all along the way, you don’t have to sell any assets to make the payments.

This may seem odd at first, but we are closer to this kind of entwined monetary system than most may think. There are new DeFi protocols that are attempting to allow anyone to borrow against their future asset yields, meaning they are creating self-paying crypto loans.

Alchemix is the most advanced of these platforms, where you can deposit crypto assets, borrow against them, and then have the future yield of these assets automatically pay off your debt. This system creates a loan where its value only goes down, and the collateral that you provide is never liquidated. The idea of self-paying loans is certainly an interesting one and may change how we think about money.

What Are Self-Paying Crypto Loans?

The concept is a new financial tool at its foundation. It’s blending both aspects of a lender and a savings account into one. You earn interest on your deposits even when you are also borrowing against them.

The interest that you earn is automatically used to pay down the loan amount, ensuring that the amount never increases, and because you are borrowing the same asset that is being used as collateral, your assets will never be liquidated.

How Self-Paying Crypto Loans Work

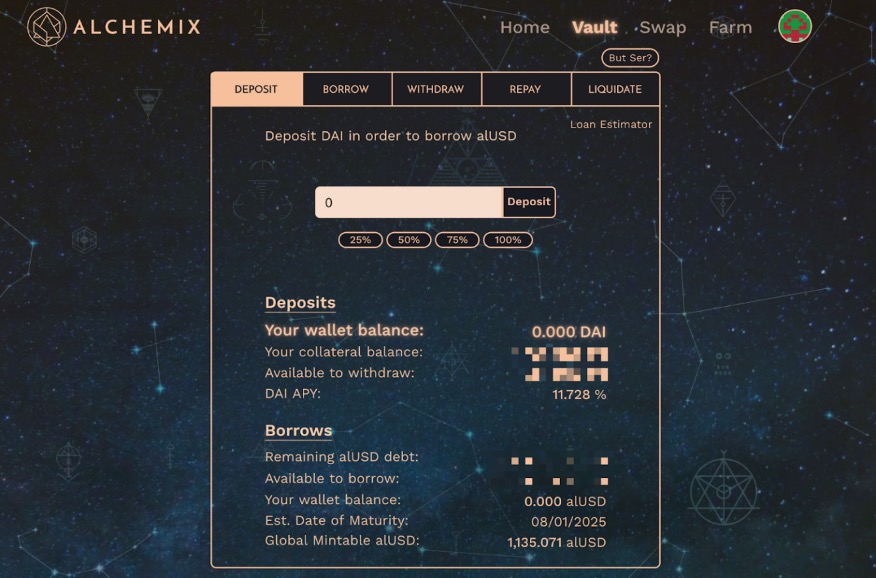

In the case of Alchemix, to use it, you must first deposit funds into the Alchemix account in the form of the popular stable coin DAI, or other assets like ETH or USDC. Dai is an Ethereum network built by stablecoin pegged to the US Dollar. The DAI that you purchase will immediately go into what Alchemix calls its “Vault,” immediately earning interest.

When funds are deposited, the account owner can immediately borrow up to 50% of deposited funds as alUSD. alUSD is also a stablecoin that has been created by Alchemix and is pegged to the USD. From there, you can take the alUSD and use it how you wish. You could cash it out as fiat USD, or you could buy another crypto such as Bitcoin or Ethereum.

Once you have your amount of capital deposited in Alchemix, and you have half of this value available to be borrowed in the form of alUSD, the thing that makes Alchemix special is that the loan amount never increases: It can only go down. Instead of the interest going to increase your deposits, it pays off your debt.

Why Are Self-Paying Crypto Loans Better?

It is easier to understand with a simple example. Let’s say you have $10,000, and the current interest rate is a fixed 10%. Let’s also assume that repayment is flexible and there will be no additional money entering the system.

With Alchemix, you can take your deposit of $10,000, and you can borrow $5,000 against it. You are earning 10% interest on the $10,000, which is $1,000 a year. The interest that you are earning on that deposited amount is going to directly pay down the loan, which is NOT accumulating interest. This means that after one year, you still have $10,000 in assets in the Vault, and the debt is only $4,000, so the total is $6,000.

Alternatively, with a traditional institution, you could deposit that same $10,000 and borrow $5,000 against it. After a year, you would have $11,000 in assets but also have $5,500 in debt (due to the 10% interest on the loan). This total would only be $5,500, not $6,000, and a 9% lower return than if the loan was obtained with Alchemix.

How Is This Possible?

The protocol is taking advantage of the larger supply of capital to pay down the smaller liability. The effective interest rate gets doubled by directly paying down the debt with the earned interest. This is similar to reducing costs for a business. Cost reduction is a more efficient way to increase the profit margin than expanding the business’s revenue.

The idea gets even better when you consider that TradFi (traditional finance) interest rates paid on assets are near-zero (or 7% using average S&P returns), but Alchemix has historically offered 10 to 20% interest on DAI (we will discuss why so high shortly).

Let’s investigate a few examples of how this can fundamentally change our relationship with money. To do so we will assume that the interest rate is a flat 10%.

Self-Paying Mortgage

Let’s assume that you are buying a home to be your primary residence, which costs $300,000. You qualify for an FHA loan that charges 4.5% interest, and you are required to pay 3.5% down. For this loan, you will only need to provide $10,500 for the down payment, but you have $25,000 in cash. You are debating whether to put all of it down or to put the sum in Alchemix.

If you put the $25,000 into Alchemix and use a $12,500 loan for the down payment, you have covered your down payment, and you have the $25,000 in Alchemix earning interest, and you can borrow against the interest. Every month you would be able to borrow an additional $208 from the debt that is being automatically paid.

This $208 could be going toward your monthly mortgage costs. At a 4.5% interest rate, you would be paying $2,091 a month. With a Vault deposit of 251,300, you could be making earned interest to cover the entire mortgage.

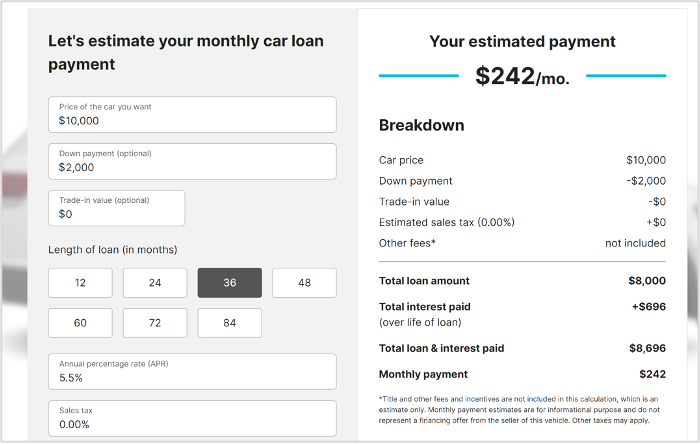

Self-Paying Auto Loan

If we are in the market to buy a used car and debating whether to pay for it with $10,000 in cash or put the money into Alchemix and get a car loan, we can use the following parameters. A credit score of 660 to 780 (considered Prime), a $2,000 down payment, an interest rate of 5.5%, and a term of 36 months.

If you deposit the $10,000 into the Vault and borrow $2,000 for the down payment, you are earning $83 a month while having to pay $242 a month toward the car loan. This is a net cost to you of $159/month. Since you have an additional $3,000 left, you could continue to draw out the $159 a month for the first 18 months (nearly 19) months before having to pay anything for the car out of pocket. And you will have your $10,000 in the Vault earning interest.

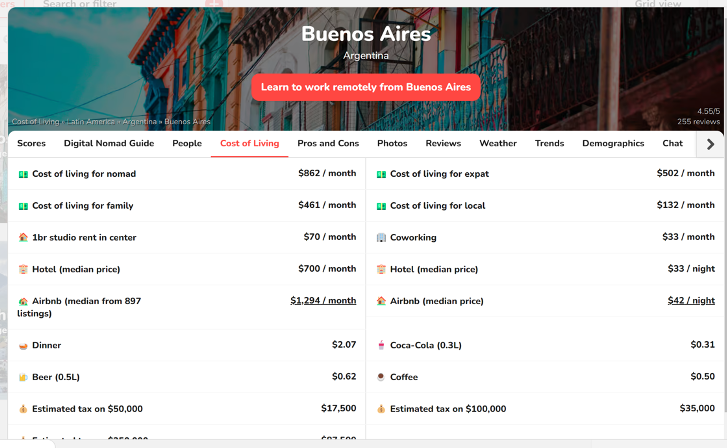

Digital Nomad Lifestyle

After working in the banking industry for years, you have saved $150,000 and want to take a year sabbatical to work on your masterpiece. You chose to put $150,000 in Alchemix. You check out possibilities and find that you can live in Buenos Aires for $862 a month.

This is significantly less than the $1,250 that you can safely withdraw. This way, your savings are completely covering your new lifestyle. What’s more, every month, you’re adding to the top line of Alchemix, so the monthly allowance is also going up. This can help account for inflation, increase your standard of living, or build a fund that supports your lifestyle.

How a Self-Paying Crypto Loan Scheme Works

Alchemix gets a slightly better rate due to their volume, but Alchemix also has a bonus DAI treasury in its “Transmuter” which also earns interest on Yearn and this interest goes to Alchemix. The Transmuter was initially used to convert alUSD back to DAI, but because Alchemix has gained popularity, the Curve pool for alUSD has also gained popularity with over 68 million alUSD, providing sufficient liquidity for Alchemix users to skip the Transmuter step entirely.

The Transmuter provides an essential service ensuring that the alUSD maintains its $1 peg, but it can do so effectively while earning interest on about 124,000,000 DAI in its current stores. This has meant that even with the recent crypto crashes, including the near-death of Terra, alUSD has stayed solid, briefly falling to $0.96 and climbing back.

This was a great test of the Transmuter’s ability to maintain alUSD’s peg and continue earning interest.

A comparable strategy is when companies earn interest on their float. Money that they can claim but do not currently need, and they are able to invest while unused.

Prepaid gift cards are an example. The current balance for Starbucks prepaid cards is at $1.4 billion. Customers could use that at any time, but Starbucks already has this cash available and they are using it to make money through investments or business expansions.

Likewise, Alchemix is putting the money to work, but the depositors are getting the upside, rather than Alchemix (or Starbucks).

Alchemix is making a profit because they are getting a higher interest rate than they are paying to their depositors. Ten percent of the profits that Alchemix earns for users is stored in the treasury and is used for paying the Alchemix team in addition to solving any bugs or issues that have come about.

This system aligns Alchemix’s incentives with those of its customers. They are only paid when providing good returns for users and are therefore incentivized to find the correct balance of return and risk.

It is deceptively simple:

1. Deposit DAI (or other allowed coins)

2. Borrow alUSD

3. Debt is repaid with Yearn Interest (now Saddle is available too)

This simple model shows how DeFi can provide new projects that are built upon each other. Alchemix is built on Yearn and Yearn on Compound, AAVE, and other apps, all of which are built on Ethereum.

Risks of Self-Paying Crypto Loans

The strength of Alchemix comes from the leveraging of other DeFi protocols. Specifically, the intelligence behind building a new lending protocol that is automatically repaid and cannot be liquidated.

However, failures of the parts below Alchemix (Yearn, Saddle, Compound, AAVE, Ethereum) in the stack could easily cascade to harm Alchemix, and there is not much Alchemix could do to fix this. Alchemix has created security systems to protect their users’ funds in an emergency event, and they have proven reliable with crypto market crashes.

Alchemix has been audited, and its V2 version has a continuous auditing system. Security is clearly a priority for the project.

Closing Thoughts

Self-paying crypto loans represent a new era of finance that will potentially bring massive changes. It gives us reason to think of money differently.

The latest projects will likely attract those willing investors who may well make great returns. This novel style of lending and borrowing opens new doors. Particularly, it opens the relatively unexplored avenue of using variable returns to pay down low- or zero-interest loans.

Disclaimer: The author of this text, Jean Chalopin, is a global business leader with a background encompassing banking, biotech, and entertainment. Mr. Chalopin is Chairman of Deltec International Group, deltecbankstag.wpengine.com.

The co-author of this text, Robin Trehan, has a bachelor’s degree in economics, a master’s in international business and finance, and an MBA in electronic business. Mr. Trehan is a Senior VP at Deltec International Group, deltecbankstag.wpengine.com.

The views, thoughts, and opinions expressed in this text are solely the views of the authors, and do not necessarily reflect those of Deltec International Group, its subsidiaries, and/or its employees. This information should not be interpreted as an endorsement of cryptocurrency or any specific provider, service or offering. It is not a recommendation to trade.